Assignment 2A: Derivative Markets, Regulation of the Banking & Securities Industry, Central Banking and Risk Management

Learning Outcomes assessed by ACFI7012 Financial Markets & Institution Assignment

● Exhibit a thorough understanding of the main theoretical frameworks which have been used to analyse developments in financial markets and of their key assumptions and methodologies

● Demonstrate skills of critical appraisal with regard to the evidence put forward to validate theoretical approaches

● Apply the theoretical and empirical knowledge obtained in the module to the analysis of the impact of financial markets and institutions on businesses using funds and the regulatory issues which arise from this impact

● Demonstrate an ability to apply academic knowledge and skills in practical contexts.

● Demonstrate an ability to engage in problem solving in ways appropriate to both participants in & regulators of the financial system.

● Demonstrate an ability to apply formal modelling techniques in the context of financial theory

Objectives Part 2A

Part A of your Second Assignment is designed to assess your attainment of specific learning objectives from the second half of the module, weeks 7 to 11 focusing upon the following areas: a. Linear and non-linear derivative instruments and how they are used to transform and mitigate exposure; b. the appraisal of how financial institutions identify, measure and manage risk; c. comparing the key features of Supervisory and Prudential Regulation of the Banking and Securities Industry; and d. the role of Central Banks as lenders of last resort.The Assignment requires you to answer both objective computational questions as well as provide discursive interpretation of your results. In total, there are three questions with sub-

parts. Together the three questions count 30% towards your overall grade for the Module and is marked on the basis of 100%.

Instructions for ACFI7012 Financial Markets & Institution Assignment

You should perform calculations, as required, for each question in an Excel Spreadsheet. The results including graphs from Excel must be copied into your word document for submission. In addition, you must upload your Excel spreadsheet to complete your submission. There should be one Word Document covering all Three Questions. There should be one Excel spreadsheet covering all three questions, having separate tabs labelled Q1, Q2 and Q3.

Q1. The Skipton Building Society, like virtually all financial institutions, views asset and liability management as a key concern. Management wish to ensure that there is an adequate spread between return on assets and the cost of funds, liabilities. They are also concerned with the interest rate sensitivity of assets and liabilities as well as their respective liquidity. A

key asset for Skipton is in the form of 30-year mortgages with floating interest rates that adjust on an annual basis. Skipt on obtains most of its funds by issuing 5-year Certificates of Deposit. It uses the Yield Curve to assess the market’s anticipation of future interest rates. It believes

that expectations of future interest rates are the main driver affecting the Yield Curve. Assume that the Yield Curve is steeply downward sloping. Based upon the information provided and your understanding of what drives their business model, please answer the following questions:

a. Why is it important to assess the sensitivity of assets and liabilities in a financial institution such as Skipton? (9 marks)

b. If the time-weighted value (duration) of assets is not the same as that of liabilities, in effect, what is the financial institution doing and explain why this may or may not be problematic. (8 marks)

c. What do we mean by Liquidity Matching and why should this be important to an institution such as Skipton? (8 marks)

d. Why or why not do you think Skipton should use financial futures as a method of hedging? (8 marks)

Q2. You manage equity investments for a hedge fund based in Mayfair. Your fund specialises in U.S. shares and plans to hold these securities over a long-period. You are worried that share markets may experience a temporary decline over the next three months and your portfolio of U.S. shares will follow the market downward, losing value. You are considering using options on the S&P 500 Index futures (options on futures) to manage your risk and there by transform or mitigate your fund’s exposure. The S&P 500 Index is trading currently at $3,000 which is the full value of the Index. The following options on the S&P Index futures are available and all expire in three months.

As information, Option Contracts on the S&P Index are for 100 units. (So, for example, on the strike price of 2800, you pay $10,800 and One Contract on a Strike of 2800 would hedge $280,000). Given the above information, please answer the following questions:

a. If your portfolio is presently valued at $8,000,000, approximately how many Index Option contracts should you use in order to hedge your entire portfolio against falling value? Please show and explain your calculations. (11 marks)

b. How would hedge your portfolio so that your approximate loss would not exceed 7% from present value? What would be the cost of such a hedge? Please explain and show your calculations. (11 marks)

c. Given your belief that the share market in the next three months may fall, how might you reduce the cost of having down-side protection. With an example, please explain and show your calculations. (Hint: What “position” in what options would correspond to a “bearish” market view?) (11 marks)

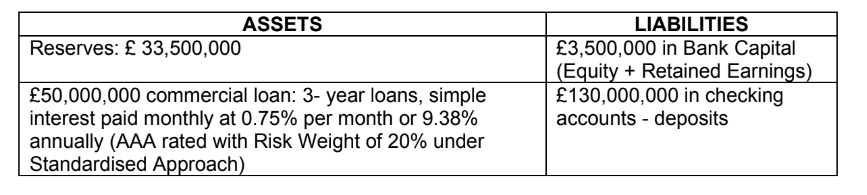

Q3. People’s Bank, a new start-up bank has begun operations with the following assets and liabilities:

Given the above facts, please answer the following questions:

a. Explain and calculate the minimum reserves the Bank must hold if Required Reserves are 10% and of what may they consist? (5 marks)

b. What are the Bank’s Risk Weighted Assets and Tier 1 Capital ratio (5 marks)

c. What does it mean for a bank to be “adequately-capitalised” and do you think People’s Bank is in that position? Please explain why. From a systemic perspective, why is it important for banks in general to have sufficient capital? (5 marks)

d. If because of Central Bank policy, mortgage rates increased to 10% how would it affect the market value of People’s mortgage book? Why? How would it affect People’s “market value” and its required capital? (5 marks)

e. What Central Bank policy might explain the increase in interest rates and, most likely, how was the increase in interest rates engineered to happen? (5 marks)

f. If Bank regulators force People’s Bank to sell its mortgages to recognise their change in market value, how would this impact the bank’s capital position? What would be the effect upon reserves? (5 marks)

g. If there were an economic panic leading to a “run on the bank” (depositors taking their money out) what impact would it have upon required reserves? What policies or measures might prevent the “run” from happening? (4 marks)

ORDER This ACFI7012 Financial Markets & Institution Assignment NOW And Get Instant Discount

Read More :-

ACFI7012 Financial Markets & Institution Assignment-Oxford Brookes University UK.