Instructions to students:

Candidates must answer all questions from the assignment.

Materials:

Dictionaries are not permitted.

Assignment: AF1101 Introductory Financial Accounting

Question 1

Printmark is a printing business set up two years ago by Mike and Jean Porter (as a partnership), when Mike was made redundant from his job as manager of a print shop. Mike does the printing and delivery work, whilst Jean, a former marketing manager, deals with advertising and administration.

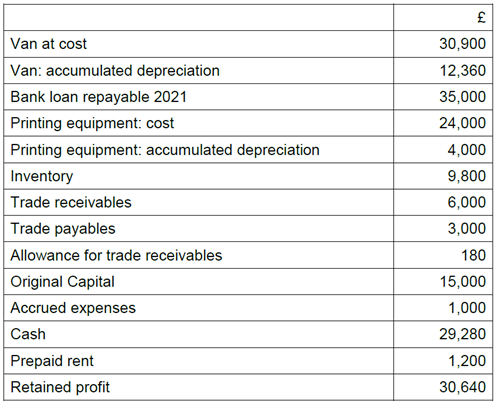

A list of closing balances as at 31st March 2016, the last day of Printmark’s first accounting period, is provided below for you:

Further information: AF1101 Introductory Financial Accounting-city university, London

- The van was bought at the start of the business on 1st April 2015. They expect it to last for 4 years, and then to sell it for £4,000. The van is depreciated at 40% per year using the reducing balance method.

- The specialist printing equipment was bought second-hand when Mike and Jean started their business. They expect it to last for 6 years and have no residual value at the end of its useful life. The straight-line method of depreciation is used for this asset class.

- Printmark rents their business premises for £400 per month, payable quarterly in advance.

- There is an accrued expense in relation to electricity amounting to £1,000 as at 31st March 2016.

- An allowance for trade receivables of 3% is maintained.

During the accounting period to 31st March 2017, the following transactions/events took place:

- The printing equipment breaks down frequently, so Mike and Jean sell it during the period for £6,000. In its place, new printing equipment costing £30,000 is bought for cash on 1st October 2016. The new printing equipment has an expected useful life of 10 years, at the end of which the residual value will be £3,000. The company’s policy with respect to depreciation is to charge a full year’s worth of depreciation in the year of purchase and no depreciation in the year of sale.

- Credit sales of £82,800 and cash sales of £23,400 are made.

- The inventory consists of printing consumables (paper, ink, etc). Further supplies costing £63,500 are purchased on credit during the year. As at 31st March 2017, inventory totals £8,100 and trade payables total £14,400.

- Receipts from trade receivables during the period totalled £80,400.

- Rent payments were made quarterly in advance on the following dates: 30th June, 30th September, 31st December, 31st March. From 1st January 2017, the monthly rent increased by 10%.

- Electricity bills totalling £3,200 were paid during the period. At the end of March, the electricity bill for the quarter March – May 2017 had not yet been received, but was estimated at £1,230 (assume electricity is consumed evenly over the quarter).

- Van expenses for the year totalled £7,600 and were all paid before the end of the period. Telephone expenses of £80 a month were paid by direct debit. Bank interest of £650 was received during the period. Annual interest of 8% was charged on the outstanding loan, half of which was paid during December 2016, with the remaining outstanding at the end of the period.

- No bad debts had been written off during the year. However, of the amounts due from credit customers at the end of the year, £2,000 had been outstanding for more than six months and it was considered that it would not be collected as the customers concerned had just filed for bankruptcy. The owners have decided to decrease the allowance for trade receivables from 3% to 2%, after writing off the uncollectable amounts, due to improving macroeconomic and industry conditions.

- Each owner withdrew £500 on the first of each month for their personal living costs.

Required:

Prepare an Income Statement for Printmark for the year ending 31st March 2017. Show clear workings of how you arrived at each income statement figure.(19 marks)

Prepare a Statement of Financial Position for Printmark as at 31st March 2017. Present detailed workings of how you arrived at each statement of financial position figure, including the closing cash balance. (21 marks) Total 40 marks

Question 2

- The following are three of the main accounting conventions used when preparing financial statements:

- The historic cost convention

- The prudence convention

- The matching principle

For each of the above, explain the convention and discuss its effect on the financial statements. Give relevant examples to illustrate your answer. (15 marks)

2.It is widely known that Assets = Equity + Liabilities; however, users often struggle to understand what the statement of financial position really represents.

You are required to explain intuitively (without the use of a formula) why the statement of financial position balances. Use an example to support your answer. (5 marks) Total 20 marks

ORDER This AF1101 Introductory Financial Accounting Assignment NOW And Get Instant Discount