Instructions: Answer all questions

Please note that there can only be one correct answer.

TASK: EC3013 Financial Economics Assignment

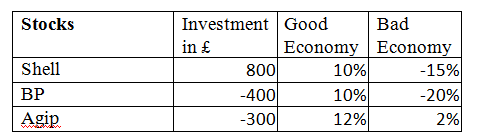

Questions 1, 2, 3, 4, are based on the following data.

1.The respective weights of the three stocks in the portfolio are:

A) 0.8, -0.4, -0.3

B) 8, -4, -3

C) 0.8, 0.4, -0.2

D) None of the above

2.If the good economy is 4 times as likely as the bad economy, the expected return on the portfolio is:

A) -6%

B) -0.006

C) 6%

D) None of the above

3.If the good economy is 4 times as likely as the bad economy, the risk associated to the portfolio is measured by:

A) variance = 4%

B) standard deviation = 2%

C) variance = 0.016

D) None of the above

ORDER This EC3013 Financial Economics Assignment NOW And Get Instant Discount

4.If the good economy is 4 times as likely as the bad economy and the portfolio is made of only BP and Agip the variance-covariance matrix is given by the following values:

A) variance(BP) = 0.04, covariance(BP,Agip) = 0.0013, variance(Agip) = 0.0064

B) variance(BP) = 0.0144, covariance(BP,Agip) = 0.0048, variance(Agip) = 0.0016

C) variance(BP) = 0.04, covariance(BP,Agip) = -0.0013, variance(Agip) = 0.0064

D) None of the above

Question 5 and 6 : EC3013 Financial Economics Assignment-City, University of London

5.Nike has an expected return of 11% and a beta equal to 8. The risk-free rate on the market is 3%. If the CAPM holds the mean return of the market portfolio is:

A) 7%

B) 4%

C) 8%

D) Need more information to answer

6.A necessary condition for the CAPM to hold is that:

A)Investors have the same preferences for risk and returns

B)Investors have the same beliefs

C)Short sales are allowed

D)Markets are strongly informationally efficient

ORDER This EC3013 Financial Economics Assignment NOW And Get Instant Discount