Unit Title : Financial Management & Cost Planning

Assessment Weighting (%): 50%

Word Count or equivalent : 2000 equivalent

Introduction

Abstract:

This paper deals with feasibility appraisal of the retirement accommodation project in Sheffield. It is proposed

to develop a small number of single bed executive homes in the Dore area of Sheffield, with development aiming to exhibit the developers’ commitment to ethical capitalism, through the attainment of a level 5 code for sustainable homes rating.The re-appraisal of the development comes in light of significant external changes. The developer now

requires an updated development appraisal for the project derived from cash flow schedules and allied techniques.

You should attend class each week as further guidance on the assignment will be given verbally on an ongoing basis.

Financial Management & Cost Planning Assignment – Sheffield Hallam University UK.

1.Introduction.

1.1 Outline

This document outlines a hypothetical speculative development scheme of ten detached single bed dwellings.

2.The Project Details

2.1 Outline

Developer: Hallam Developments Ltd

Number of Units: Ten (Phase One)

Location: Dore, Sheffield.

Site Area: One Hectare.

The land for this development scheme was purchased immediately before the project commenced. It is situated in a residential area within Dore..

The site layout with plot numbers is illustrated in Figure No 1 below.

The site was purchased with outline planning permission although detailed planning permission was not yet applied for. No difficulties were anticipated from the planning department since the scheme was generally within the terms of the local plan and supplementary planning guidance for the locality whilst also meeting the assumption in favour of sustainable development principles outlined in the planning policy framework.

No significant problems were expected with the site. It was clear of existing buildings and contained no other complications such as tree preservation orders.

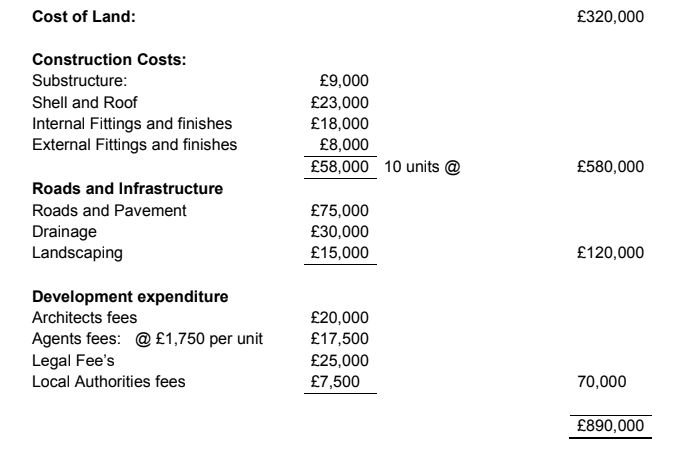

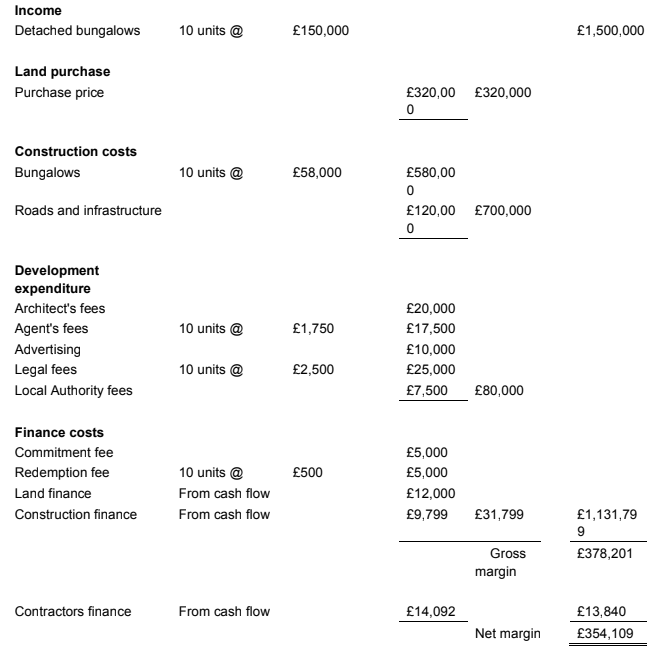

2.2 Cost of Land and Construction

The Main cost headings – apart for finance – are listed below:

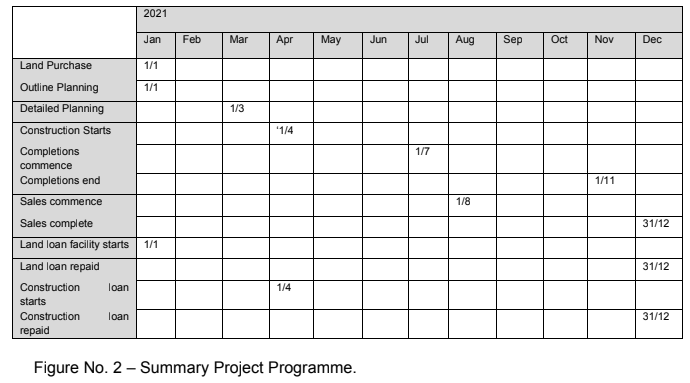

2.3 Developers Programme :

The intended development programme starts on 1st January 2021 and is scheduled to finish by the start of December 2021. The land is to be purchased at the start of January with outline planning permission. Detailed planning permission is expected by 1st March and construction is expected to commence on 1 st April. The first houses were due to be complete by the end of July and sales could commence from 1st August. The completions and sales were expected to proceed at a rate of two per month until the end of the year.

2.4 Finance:

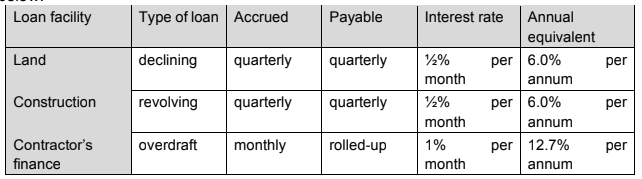

The scheme is partially funded by a financial institution over a one year period. The loan facility is valid until the end of 2021. The interest charged is 1⁄2% above minimum lending rate (assumed to be 51⁄2%), which can be taken at 6% per annum or 1⁄2% per month simple interest. The interest charged on the loan facilities is levied on a quarterly basis in arrears and is paid out of the developer’s cash flow. It has to be paid over the end of each quarter and is not ‘rolled up’.

Banks and institutions have had their fingers burned in the past by loaning 90% or even 100% of spending on land and construction during periods of boom and bust in the 1970 s. In the event of the developer becoming insolvent, the funding body will be dependent on either completing the project or selling off the land and built assets to recoup their outlay.

They now tend to restrict funding to 80%/80% on land and construction respectively. In this case it is funded on a 75%/75% basis. Financial institutions are also reluctant to finance ‘intangible’ expenditure such as Architects and Quantity Surveyors fees, legal costs, etc. as they do not regard them as real security.

The land is funded on a reducing basis with the loan limited to two-thirds of the purchase price. This comes to £320,000 75% = £240,000 and is repayable at £24,000 per house sold.

The construction costs are funded on three-quarters of the costs. This is on a revolving basis. Thus, finance is released; amounting to 75% of construction costs each month and is repaid as units are sold. This amounts to a theoretical maximum of (£580,000 + £120,000 = 700,000) 75% = £525,000. It is inevitable that some will be repaid by the time the full costs are incurred. On each sale £525,000/10 = £52,500 will be repaid.

The remaining £80,000 of the land cost and the balance of the construction costs plus all the other development expenses and loan interest payments are carried by Hallam Developments from their own cash flow. Any cash flow deficit must be covered using a bank overdraft facility. This is rolled-up monthly at the current compound rate of 1.0% per month, this approximates to an annual rate of 12.7%.Details of the various loan and overdraft facilities available are presented in Figure No 5 below:

Figure No 5: Loan and overdraft facilities

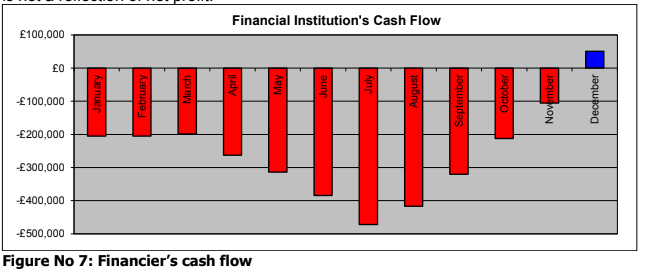

2.5: Cash flow

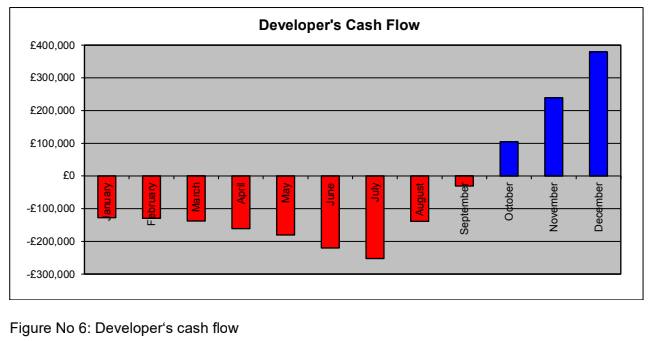

The projected payments and repayments schedule for the project is presented in Table No 1.The cash flow schedule for Hallam Developments and the financier are given in Table No 2. These cash flows are presented graphically in Figure No 6 and Figure No 7.

2.6: Developer’s Budget

The developer’s budget for the project is given below. This relies on information on interest payments on the loan and overdraft facilities from Table No 2.

2.6: Developer’s Budget

The developer’s budget for the project is given below. This relies on information on interest payments on the loan and overdraft facilities from Table No 2. This illustrates that the scheme is expected to produce a reasonable return. The projected surplus of around £350,000 represents a margin of nearly 25% on the £1,500,000 turnover. It represents an

even more impressive looking projected return of 135% of the maximum financial commitment of Hallam Developments of just over £260,000 in July 2021. It should be emphasized that the project will have to be allocated a share of Hallam Development’s overhead costs so the net margin reported is not a reflection of net profit.

3: Construction

3.1: Problems encountered

A number of problems were encountered with the project:

❑ The first difficulty encountered was that there was a delay in the grant of detailed planning permission Additional infrastructure costs were required to meet the local authority terms. This delayed the start of construction work.

❑ Inflation in construction costs results in the increased cost of each bungalow while the road and additional infrastructure costs increased.

Financial Management & Cost Planning Assignment – Sheffield Hallam University UK.

❑ The strength of the local housing market had been under/over-emphasized in the original developer’s budget. This was expected to affect both the speed of sale of houses.

❑ The advertising budget was amended to help speed sales.

❑ There was a change in interest rates. This affected the inter-bank lending rate and hence the rates changed by the financial institution for the loan and the bank on any overdraft.

3.2: Response from the Developer

The developer responded to the lower/higher than anticipated demand by inspecting the asking price for the dwellings.The anticipated sales rate was revised upwards/downwards. Even this rate of sales required revised

advertising and promotion expenditure.The delay in the grant of detailed planning permission and the slower/higher expected sales pattern meant that the original loan facility agreement was no longer applicable. The Developer was forced to renegotiate the arrangement.

Please note the above problems apply to a certain set of criteria. You need to adjust the above in line with your specific set of criteria.

3.3: Revised terms of the loan

The Financial Institution agreed to extend the period of the arrangement to cover the revised. They were reluctant to fund the increased costs of construction. Therefore they reduced the funding to 70% of the revised construction costs from the original 75% to keep their outlay the roughly in line.Thus the Developer had to carry the increased construction costs out of their own cash flow. This had the effect of increasing the call on the overdraft facilities.

The interest rates were increased to reflect the higher base rates and the longer period of the loan.

The bank also increased its interest rate on the overdraft facility up to 11⁄2% per month (19.6% per annum) to reflect the higher general rates and the increased perceived risk given the above points.

Financial Management & Cost Planning Assignment – Sheffield Hallam University UK.

4: Tasks

4.1 Overview of assessment problem.

The out-turn of the project is subject to things going wrong, this includes:-

I. A delay in granting planning caused the project to commence later than planned. In turn leading to increased construction costs and an increase in the period of the loan for the purchase of the land. It has also resulted in houses being completed outside the anticipated selling window.

II. Due to the ‘credit crunch’ interest rates increased / decreased from those included in the feasibility study. This affected both the loans to cover the cost of purchasing land and construction costs from the finance company and the cost of overdraft facilities.

III. The sales rate of the houses was much slower / quicker than anticipated and the prices had to be inspected accordingly as the marketability of the location had been over / under-estimated.

4.2 Assessment Tasks

Produce a modified proposal reflecting the financial position of the project after the following cost fluctuations and time delays resulting (i) a delay in obtaining detailed planning permission, (ii) a general rise / fall in interest rates, (ii) rising costs of construction and finally (iv) difficulties/successes in selling completed houses.

Financial Management & Cost Planning Assignment – Sheffield Hallam University UK.

You should:

a) Use the information to produce a revised cash flow schedule for the development and updated developers budget;

b) Compute the revised outcome in terms of profit and loss;

c) Identify the factors responsible for the change in the above giving the contribution of each.

d) Provide advice on approaches which could be implemented to reduce the chance of future misleading development appraisals

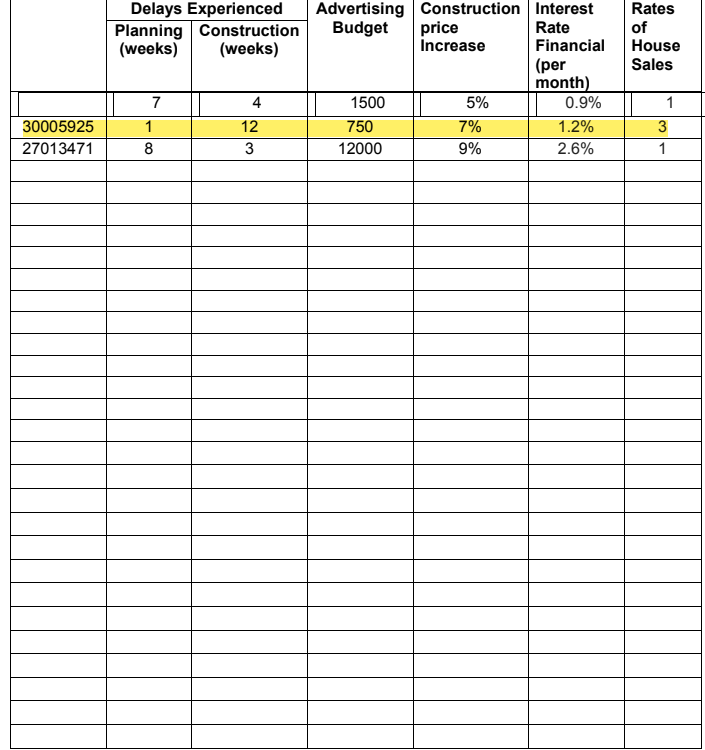

4.3. Specific data for each learner.

The table below provides data relating to the following variations to the development appraisal.

✓ The length of the delay in granting the project planning permission;

✓ Increases/decreases in interest charges on both the loan and overdraft;

✓ Revised advertising budgets

✓ Construction price increases

✓ Speed of sales.

✓

The figures have been randomly generated and should be taken from the row corresponding to your student number which is displayed on your student ID card.

ORDER This Financial Management & Cost Planning Assignment NOW And Get Instant Discount

Read More :-