Subject Code & Title :- UFMFUG-15-3 Financial Mathematics

Assignment Type :- Assignment

Instructions to Students:

There are four questions in the paper. You must answer all questions.

Your answers must be clear concise consistent and complete. Solutions that exhibit un clear in consistent or incomplete methodology will not receive full credit.

You may evaluate the cumulative density function for the standard normal distribution using the tables provided or a suitable software package. No penalty will be incurred for the difference in values obtained between tables and software.

UFMFUG-15-3 Financial Mathematics Assignment-UK

Question 1

A financial asset is currently valued at 775p per share. A dividend payment of 25p per share is expected to be paid after six months have elapsed. The risk-free interest rate is 3.5% per year with continuous compounding.

(a) Describe the transactions that take place for the holder of a 1-year forward contract.

(b) For the holder of a 1-year forward contract determine the value per share of the contract at the following points in time.

(i) At the start of the contract

(ii) When the contract expires given that the share price has fallen to 750p per share.

(iii) After 5-months have elapsed given that the share price has risen to 785p per share.

(c) Describe the trades a trader could make to achieve a risk-free profit from a market price of 778p per share for the delivery price of a 1-year forward contract. Calculate the risk free profit per share.

UFMFUG-15-3 Financial Mathematics Assignment-UK

Question 2 :-

(a) Explain how the construction of a risk-free portfolio enables the price of a derivative contract to be estimated from a single step Binomial tree

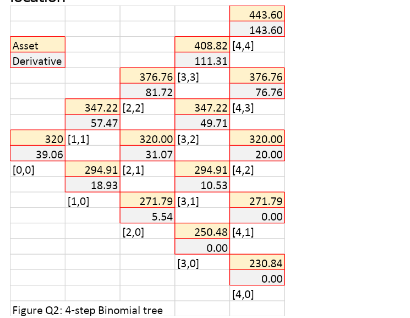

(b) A 4 step Binomial tree is used to estimate the price of an 8 month European style call option.

The asset is the share price for a financial asset currently valued at 320p per share The risk free interest rate is 5% per year with continuous compounding and the asset price volatility is 20% per year. The exercise price is equal to 300p per share. No dividends are paid during the contract.

Figure Q2 shows the Binomial tree with the values for the cells calculated to two decimal places of accuracy The asset values are denoted and the derivative values at each location

(i) Using the data provided, give two different calculations to verify the value of.

(ii) Using the data provided, verify the value of and.

(iii) For any path that terminates at location [4, 2], demonstrate the different financial out comes for the writer of the option contract when using each of the following approaches to hedging risk. Describe the trades that take place at each stage of the hedge and explain which of the strategies is the more effective with reference to the risk associated with each out come.

A static delta hedge

A dynamic delta hedge.

Assume that the contract is for 100 shares and round each trade to the nearest share.

UFMFUG-15-3 Financial Mathematics Assignment-UK

Question 3

(a) A non dividend paying asset has a current share price of per share The expected rate of growth is 8% per year the annual volatility is 20% per year and the risk free interest rate is 2% per year with continuous compounding.

A trading strategy is created whereby the trader

Sells 1 out-of-the-money put option contract (exercise price

Sells 2 in-the-money call option contracts (exercise price

Buys 2 at-the-money call option contracts (exercise price

Note: The out-of-the money put option and the in-the-money call options have the same exercise price

where

All contracts are six month European style options and each contract is for one share Selecting suitable values for the exercise prices and

(i) Describe the trades that are implemented for different values of the underlying asset at expiry.

(ii) Calculate the probability of a profit from this strategy. Please provide details of all calculations together with any relevant pay-off and profit diagrams required to answer this question.

(iii) Describe the main features of the strategy and explain how it is designed to take

advantage of specific market conditions

UFMFUG-15-3 Financial Mathematics Assignment-UK

Question 4

(a) A discrete time stochastic process is defined by denotes the change in over a time interval and .

Using generate a single path of over a 1 year interval from an initial value of and the standard normal variate sequence

Note that

(b) A financial asset follows a lognormal distribution over a time interval such that

where is the current asset price is the expected growth rate per year and is the volatility per year.

(i) A European style derivative contract is created that returns the value of the function

at expiry. Assume that the contract returns the numerical value of the function in

pence (p). Determine the analytical pricing formula for the above derivative contract.

(ii) Modify the pricing formula obtained in (b) part (i) so that it is valid for an asset that returns a continuous annual dividend yield.

(iii) The current value of a financial asset is 850p per share and returns a continuous

dividend yield of 6% per year the risk free interest rate is per year with continuous

compounding and the asset price volatility is 15% per year. Calculate the price of a six month contract and compare this value with an estimate obtained from a one step Binomial tree.

ORDER This UFMFUG-15-3 Financial Mathematics Assignment NOW And Get Instant Discount

Read More :

6008LBSBSC Strategic Corporate And Project Finance Assignment – UK