CW1 Part 2 (60% of CW1 and 30% of the total overall module mark)

You need to imagine that you have borrowed a total of £1,000,000 at 2% interest p.a. in perpetuity and that you have invested in the portfolio given in the excel spreadsheet titled 6EC501 CW1 EEC 14 August.

6EC501 CW1 Coursework CW1 Part 2 Assignment-Derby University UK.

In the report (1500 words +/- 10%)* you will have to

Analyse your portfolio choices from a behavioural perspective and

Evaluate the asset allocation adopted applying the portfolio theory concepts studied.

Include a discussion of the purpose of the portfolio (i.e. long-term personal retirement savings) and how you believe that your portfolio fulfils the stated aim better than other possible portfolios. The report must discuss the biases that may have influenced your choice of assets – look at the reasons listed under our given portfolio tracking sheet. You must then make explicit reference to portfolio theory and analyse the portfolio allocation. Indicate how you think that your portfolio performance should be judged or bench marked over the long-term and address whether the portfolio in its reduced state (see details below) will serve your retirement goal after paying back the loan with interest. Below is a step-by-step guide to the report including the marking criteria.

Summative Feedback – you will be provided with summative feedback within 3 weeks of the final Aug EEC submission deadline of 14 th August 2020 11.59 pm.

You must stay within 1650 words – going over the max limit will result in the following penalties:

i. 10 marks deducted for exceeding the word limit by up to 250 words

ii. 20 marks deducted for exceeding the word limit by 251-500 words

iii. 30 marks deducted for exceeding the word limit by 501-750 words

iv. 50 marks deducted for exceeding the word limit by more than 750 words.

Build your Excel spreadsheet

1.Start with the portfolio Excel spreadsheet used for tracking the performance of your given investments between 1 and 28 February 2020. Add a new worksheet (a new tab) in your Excel file with your portfolio of 10 assets. Copy the entire sheet containing the tracked portfolio and paste it in the new worksheet. In the newly added worksheet, change the amounts invested in each asset to £100,000 (so that now they have equal weights in the portfolio).

2.Add a new worksheet (a new tab) in your Excel file with your portfolio of 10 assets.

a. Use the Yahoo! Finance to look up and download historical prices for your 10 assets – monthly data for the last 5 years. Put these in one single Excel sheet (just like I have done for the seminars)

b. Calculate the expected rate of return for each asset (mean) and its risk (standard deviation)

c. Calculate the correlation matrix for your 10 assets.

6EC501 CW1 Coursework CW1 Part 2 Assignment-Derby University UK.

3.You will now build 2 different portfolios:

a. Portfolio A – pick your best 5 assets using Markowitz criteria; give weights to your 5 assets in a way similar your initial allocation – i.e. increase the weights of the remaining 5 assets by the amount ‘freed-up’ by the removal of five assets.

b. Portfolio B – pick the top 5 highest performing assets from your 1-month tracking sheet; give the following weights to your assets in descending order 35% (to the asset with highest return), 30%, 20%, 10% and 5% (to the asset with the lowest return).

4.Add a new worksheet (new tab) into your Excel file for each portfolio (A and B) and copy the historical data for the 5 chosen assets for each portfolio separately. For each Portfolio A and portfolio B:

a. Calculate the expected portfolio return and the portfolio risk (Markowitz equations)

b. Calculate the portfolio beta.

c. Calculate the Sharpe ratio assuming a risk-free rate of return equal to 0.5%.

Copy and paste the Excel sheets in an Appendix at the end of your written analysis. Please do this BOTH with the results showing AND with the Excel formulae showing (use CTRL+` , the key next to 1).

Analyse the portfolio in Word document

5.You must first analyse your given investment portfolio from a behavioural perspective. Use around 500 words to discuss the biases that (may) have influenced the choice of assets – look at the reasons listed for picking the investments in the portfolio tracking sheet. Typical biases to consider are overconfidence, representativeness, availability, ambiguity aversion, narrow framing, herding etc. You will need to cite literature sources (with references at the end) in the discussion.

6.Next you must evaluate your portfolio asset allocation by applying portfolio theory (around 1000 words). You will need to cite theory and literature sources (with references) in the discussion.

7.First look at the initial 10-asset portfolio and

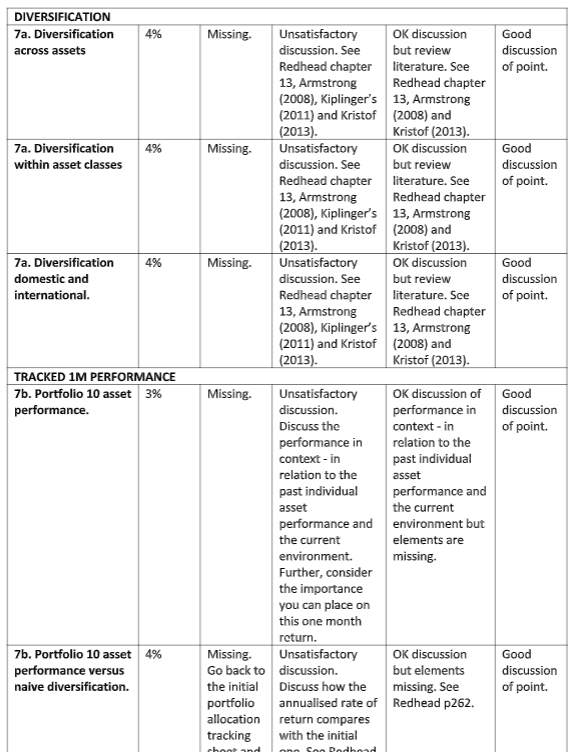

a. Analyse the diversification of the initial 10-asset portfolio

i. How well diversified was it across asset classes? How could you improve it?

ii. How well diversified was it within the asset classes? How could you improve it?

iii. How well diversified was it across international and domestic? How could you improve it?

b. How did your portfolio perform over your investment period (the month between 1-Feb and 1-Mar)? Would a naïve diversification strategy have yielded better a better result (see the equal weights portfolio)?

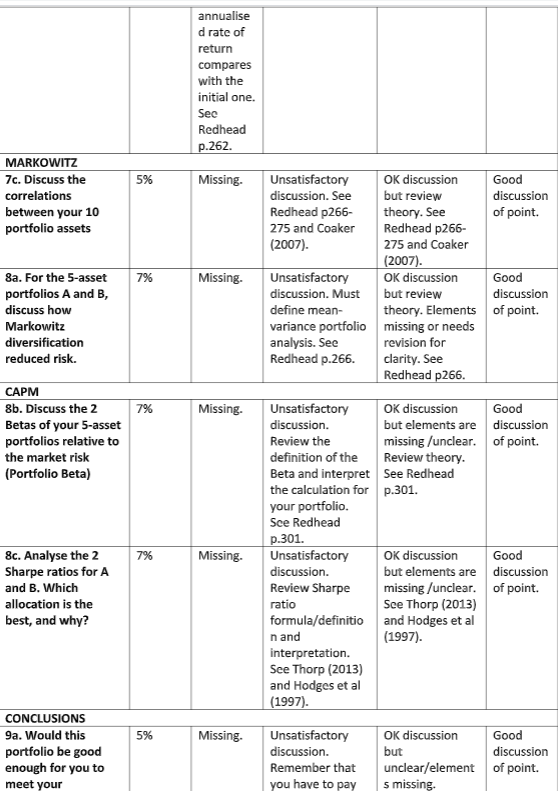

c. Discuss the correlations between your 10 portfolio assets – refer to the matrix (point 2.c.)

8.Comparing Portfolio A and Portfolio B,

a. discuss whether Markowitz diversification helped reduce risk (refer to the calculations in point 4.a.)

b. discuss the portfolio betas you calculated (point 4.b.) relative to the market risk.

c. discuss the Sharpe ratios you calculated (points 4.c.). Which allocation is the best – Portfolio A or Portfolio B, and why?

6EC501 CW1 Coursework CW1 Part 2 Assignment-Derby University UK.

9.Going back to your initial 10-asset portfolio,

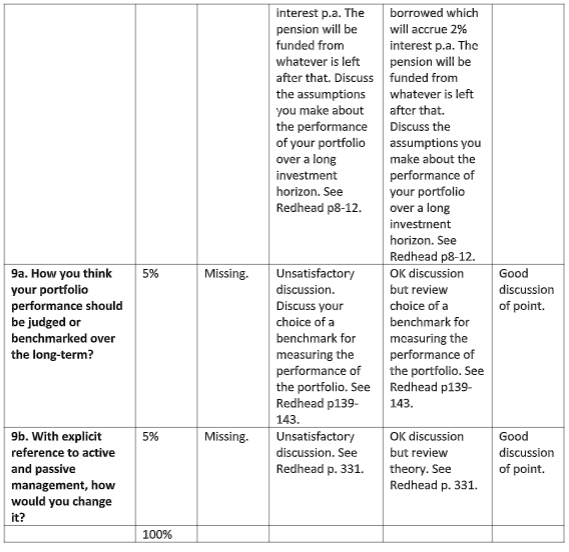

a. Would this portfolio be good enough for you to meet your retirement goal? Indicate how you think your portfolio performance should be judged or bench marked over the long-term.

b. With explicit reference to active and passive management, how would you change it?

Submit the Word document online using the Turnitin link provided. Deadline Sunday 8 th March 2020 11.59 pm

6EC501 CW1 Coursework CW1 Part 2 Assignment-Derby University UK.

ORDER This R/617/1686 6EC501 CW1 Coursework CW1 Part 2 Assignment NOW And Get Instant Discount

Read More :-